All Categories

Featured

Table of Contents

That normally makes them a more cost effective option forever insurance coverage. Some term policies might not keep the costs and survivor benefit the same gradually. You don't want to erroneously assume you're acquiring degree term insurance coverage and after that have your survivor benefit modification in the future. Lots of people get life insurance policy protection to aid economically secure their liked ones in instance of their unforeseen death.

Or you might have the alternative to transform your existing term insurance coverage right into an irreversible policy that lasts the remainder of your life. Various life insurance policy policies have possible advantages and disadvantages, so it's crucial to understand each before you determine to acquire a plan.

As long as you pay the premium, your beneficiaries will get the death benefit if you pass away while covered. That claimed, it's vital to keep in mind that most policies are contestable for two years which implies protection might be rescinded on death, ought to a misrepresentation be found in the application. Policies that are not contestable usually have actually a rated survivor benefit.

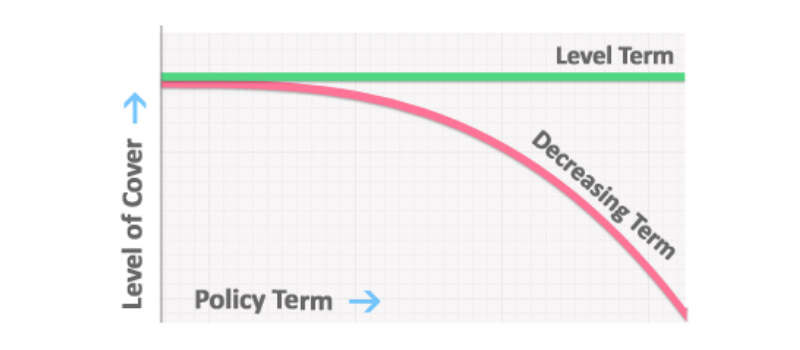

Premiums are normally less than entire life plans. With a degree term policy, you can pick your coverage quantity and the plan length. You're not secured right into an agreement for the remainder of your life. Throughout your plan, you never need to stress over the costs or death benefit amounts altering.

And you can not squander your policy during its term, so you won't receive any financial advantage from your previous protection. As with various other kinds of life insurance coverage, the price of a degree term plan depends on your age, insurance coverage requirements, employment, way of life and health and wellness. Generally, you'll locate more budget-friendly protection if you're more youthful, healthier and less risky to guarantee.

High-Quality What Is Voluntary Term Life Insurance

Considering that level term costs stay the very same throughout of protection, you'll understand exactly how much you'll pay each time. That can be a big assistance when budgeting your costs. Level term insurance coverage also has some versatility, allowing you to customize your plan with added features. These typically come in the form of riders.

You might need to satisfy specific conditions and qualifications for your insurer to enact this cyclist. In enhancement, there may be a waiting period of as much as six months before taking result. There also can be an age or time restriction on the insurance coverage. You can add a child rider to your life insurance plan so it additionally covers your kids.

The survivor benefit is generally smaller, and protection usually lasts till your kid transforms 18 or 25. This cyclist may be a more affordable means to assist guarantee your youngsters are covered as motorcyclists can frequently cover multiple dependents simultaneously. As soon as your kid ages out of this coverage, it might be feasible to transform the motorcyclist right into a brand-new policy.

The most usual type of irreversible life insurance coverage is whole life insurance policy, however it has some key distinctions contrasted to level term protection. Below's a fundamental introduction of what to think about when contrasting term vs.

Family Protection What Is Decreasing Term Life Insurance

Whole life entire lasts insurance coverage life, while term coverage lasts protection a specific periodDetails The premiums for term life insurance are normally lower than whole life insurance coverage.

One of the major attributes of level term protection is that your costs and your fatality benefit don't alter. You might have protection that begins with a fatality benefit of $10,000, which could cover a home loan, and then each year, the fatality benefit will lower by a set quantity or percentage.

Because of this, it's frequently an extra economical sort of degree term coverage. You might have life insurance policy through your employer, but it may not be adequate life insurance for your requirements. The primary step when purchasing a policy is establishing just how much life insurance policy you need. Think about factors such as: Age Household size and ages Employment status Revenue Financial debt Way of living Expected last expenditures A life insurance policy calculator can help establish just how much you need to begin.

After making a decision on a plan, finish the application. If you're approved, sign the documentation and pay your first premium.

A Whole Life Policy Option Where Extended Term Insurance Is Selected Is Called

Lastly, think about scheduling time every year to evaluate your policy. You might desire to update your beneficiary details if you've had any considerable life changes, such as a marital relationship, birth or separation. Life insurance policy can in some cases feel challenging. Yet you do not need to go it alone. As you discover your alternatives, take into consideration discussing your needs, desires and worries with a financial professional.

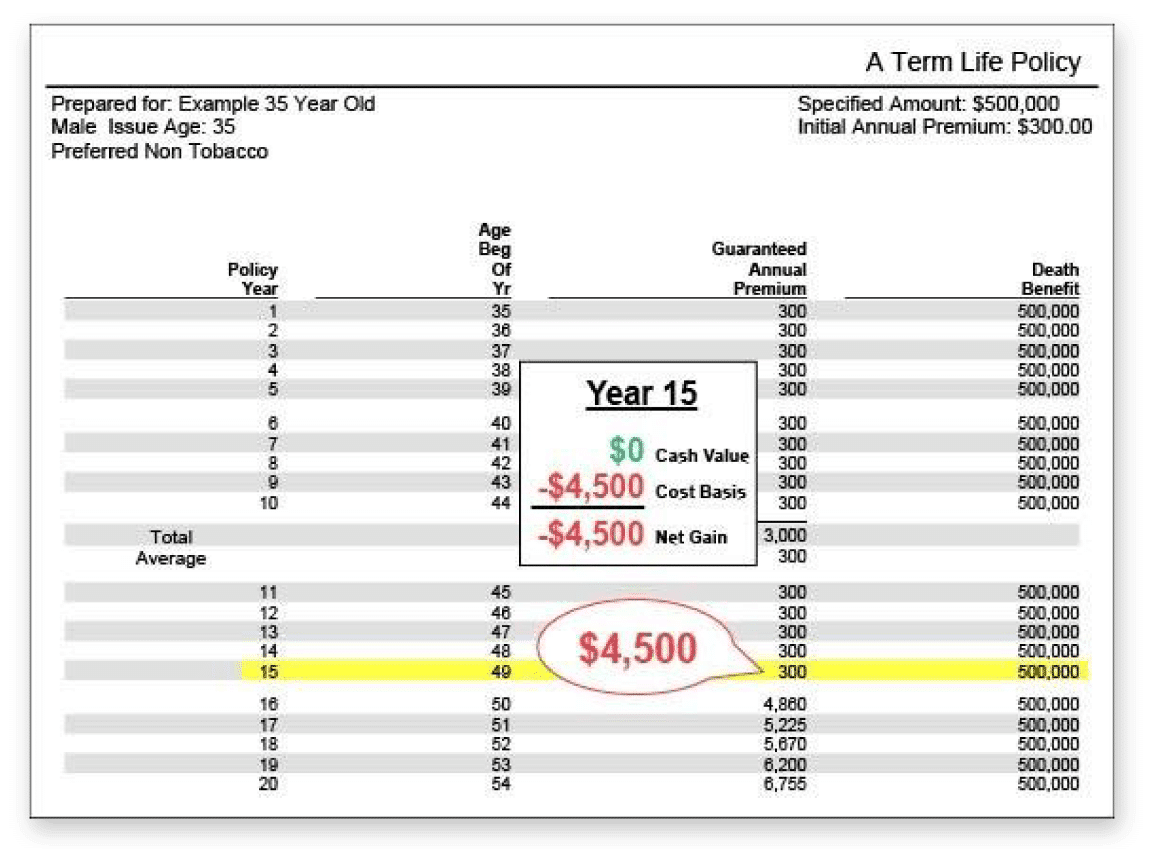

No, degree term life insurance policy doesn't have money value. Some life insurance policy plans have an investment function that permits you to develop cash value gradually. A portion of your costs payments is alloted and can gain interest over time, which expands tax-deferred throughout the life of your coverage.

You have some options if you still want some life insurance protection. You can: If you're 65 and your insurance coverage has run out, for example, you may desire to buy a new 10-year degree term life insurance coverage plan.

Best Level Term Life Insurance

You might have the ability to convert your term coverage right into a whole life plan that will last for the rest of your life. Many types of level term policies are convertible. That indicates, at the end of your protection, you can convert some or all of your plan to whole life coverage.

Degree term life insurance policy is a plan that lasts a set term normally between 10 and 30 years and comes with a degree fatality advantage and degree costs that remain the very same for the entire time the plan is in impact. This implies you'll know exactly just how much your settlements are and when you'll need to make them, enabling you to budget plan as necessary.

Level term can be a wonderful choice if you're looking to buy life insurance policy protection for the initial time. According to LIMRA's 2023 Insurance Barometer Research, 30% of all grownups in the United state need life insurance and don't have any type of type of policy. Level term life is predictable and cost effective, that makes it among one of the most preferred kinds of life insurance policy.

{kind=link}

Latest Posts

New York Life Final Expense

Instant Insurance Life Mortgage Online Quote

Instant Term Life Insurance Quotes